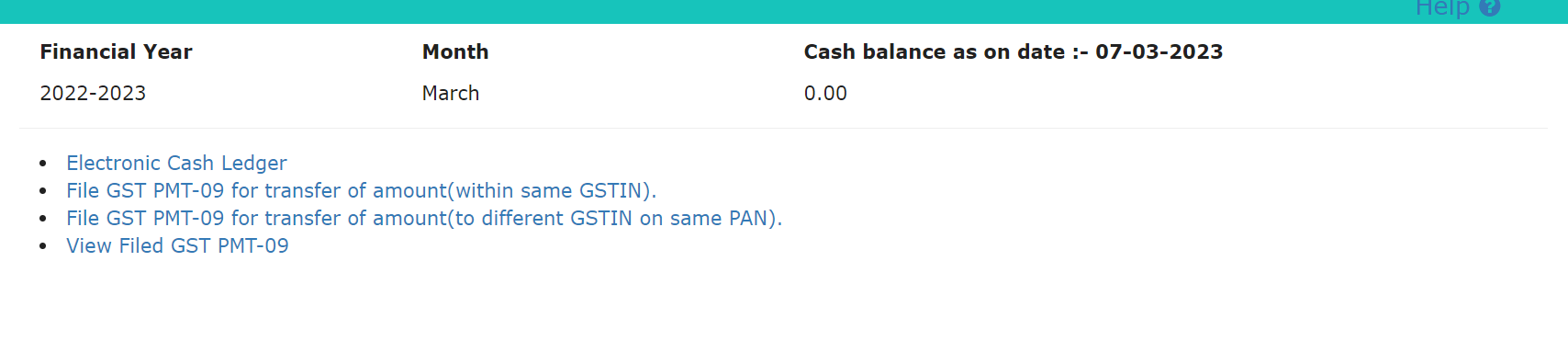

The Goods and Services Tax Network has enabled the option to transfer and utilize the amount in the cash ledger for central tax or integrated tax of a distinct person as specified in sub-section (4) or, as the case may be, sub-section (5) of section 25, in FORM GST PMT- 09.

Rule 87(14) of the Central Goods and Services Tax Rules, 2017 provides the following:

(14) A registered person may, on the common portal, transfer any amount of tax, interest, penalty, fee or any other amount available in the electronic cash ledger under the Act to the electronic cash ledger for central tax or integrated tax of a distinct person as specified in sub-section (4) or, as the case may be, sub-section (5) of section 25, in FORM GST PMT- 09:

Provided that no such transfer shall be allowed if the said registered person has any unpaid liability in his electronic liability register.